fjrigjwwe9r3SDArtiMast:ArtiCont

be frustrating. After all, what can be worse than waiting for your own money to come back to you? This is why financial advisers suggest planning one’s taxes well in advance and avoid overpayment. The start of the financial year is, perhaps, the best time to do so. Submit the Forms 15G or 15H right away to avoid the tax deducted at source (TDS) on your investments, if your income is below the exemption limit. From this year onwards, the Income Tax Department has introduced some changes in the two forms.

You now have to give additional information on income from all sources and tax deduction availed of during the financial year. According to the TDS rules, if interest income exceeds Rs 10,000 in a year, 10% tax will be deducted at source. If the investor has not furnished his PAN details, the TDS rate will be higher at 20%. However, if the investor’s total taxable income is below the basic exemption limit, he can submit a declaration to avoid TDS. Form 15G is to be used by individuals below 60 years, HUFs and trusts, etc.

Senior citizens and those above 80 years must use Form 15H. Till now, one only had to declare in the form that one’s income was below the taxable limit and, therefore, the TDS should not be deducted. Now, however, one must also mention the expected taxable income in the financial year. This includes income from all sources, such as salary, interest, rent and capital gains. One can avoid the tax-free income like interest from the PF, the PPF and tax-free bonds.

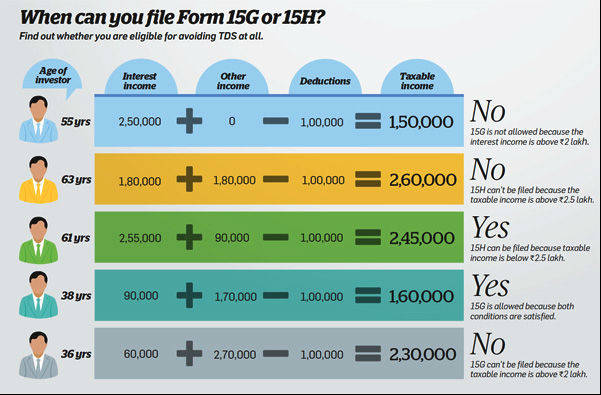

Are you eligible?

Before you rush to submit the Form 15G or 15H, make sure that you are eligible. An individual or HUF must satisfy two conditions. First, the estimated taxable income for the financial year should be less than the basic exemption limit. This is Rs 2 lakh for individuals below 60 years and HUFs, Rs 2.5 lakh for senior citizens, and Rs 5 lakh for very senior citizens above 80 years. The second condition, which is applicable only to Form 15G, is that the total interest income from all sources should not exceed the basic exemption limit. Senior citizens have been exempted from this condition because most retirees get the biggest chunk of their income from interest.

These conditions are not new. The only difference is that now the individual has to specifically mention his expected income in the form. In the table below, we look at the various situations in which an individual is eligible to file the declaration. Interestingly, these forms also require the individual to mention details of other incomes, including dividends from shares and mutual funds. Dividend income is tax-free but the Income Tax Department still wants to know how much you earned from them. "The new forms seem to have been made with all the possible situations in mind. As of now, the dividend is tax-free, but may be taxable in the future,’’ explains Sandeep Shanbhag, director, Wonderland Consultants.

|

|

Err on the side of caution The TDS rules can be cumbersome, but you just have to take them in your stride. The Forms 15G and 15H have to be submitted at every branch of the bank where you have a deposit. Though the threshold limit of Rs 10,000 a year is per branch, some banks insist on a form to be submitted even when the interest is less than Rs 10,000 in that branch.

A bank can track you using the unique customer ID. If the combined interest in all branches is above the Rs 10,000 limit, TDS will be deducted if you have not filled the Form 15G or 15H. It is best to provide the form than risk TDS. Once the tax has been deducted, it can only be reclaimed by filing your income tax return. The worst affected are investors who are not eligible to file Form 15G because their interest income is above the threshold limit even though their total taxable income is not liable to tax. One option for such people is to allow the banks to deduct the TDS. They can then reclaim the amount by filing their tax returns.

This is a cumbersome process and, therefore, not worth undertaking. The second option is to split the fixed deposits across several banks and branches so that the TDS exemption limit is not breached. This is no less tedious because you will have to go to multiple locations. Besides, it increases your paperwork manifold. There may also be cases of a small tax liability which makes an investor ineligible for filing these forms. You can handle this by letting one bank deduct the TDS so that the amount takes care of your total tax liability.

However, note that the above strategies are only meant to avoid TDS, not avoid tax or file your tax return. You may be required to file your tax return if your total income before the deductions is above the basic tax exemption limit. Besides, there is a stiff penalty for furnishing incorrect information in the form just to avoid the TDS.